The Rise and Fall of Proteus Digital Health

Mar 26, 2024

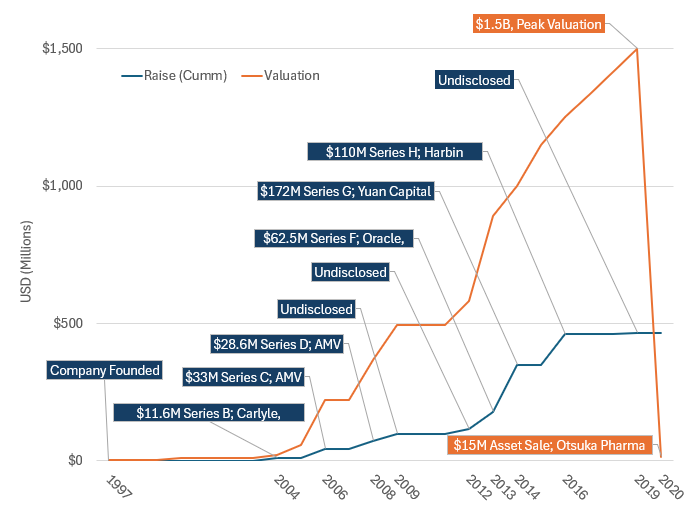

You’ve probably heard of Proteus. mAt one time it was the darling of digital health. But within a single year, Proteus went from a $1.5B valuation to a fire sale at $15m. Here's a recreation of events:

- Proteus launched circa 1997

- Over a 20-year span, they raised just under $500M

- At its 2019 peak, they carried a $1.5B valuation

- In 2020, Proteus tanked and sold assets to Otsuka Pharma for $15M

Plot showing Valuation (orange) and Cumulative Funds Raised (blue) for lifespan of Proteus. Data pulled from CrunchBase and other sources listed below. Some data values extrapolated where undisclosed.

Proteus’ Vision and Business Model

We'll get there, but maybe you're not familiar with the Proteus story during its glory days.

Proteus was in the business of pills with brains. These pills knew when they were ingested and communicated such to patches worn by patients. The patches then pushed data to smartphones, which then sent the data to the cloud.

If grandma forgot to take her pills, Big Brother would know. Maybe her iPhone would start beeping and buzzing. Maybe she’d get a reminder call from her doc. The goal and vision? Improved medication adherence -- a problem well known in healthcare.

Proteus' business strategy? Pharma brings the drugs, Proteus brings the sensors and patches. A combo product made in heaven.

But, did it work?

Several drug partnerships and developments were underway at Proteus, but the initial launch was with Otsuka Pharma, combining Proteus smartpatches and sensors with Otsuka's aripiprazole tablets. The combo was branded Ablify Mycite (AM).

Targeting Individuals with Schizophrenia

Why schizophrenia? Low medication adherence. To the tune of 58% adherence rate. (Haddad, 2023)

AM worked indeed. During a 6-month prospective study, it demonstrated a 26.5% improvement in medication adherence. Furthermore, it resulted in a 21.3% reduction in psychiatric hospitalizations. (Cohen, 2022)

Clinical Value Prop Delivered. Box Checked.

So, if it was working clinically, why did Proteus dive bomb? Well, it depends who you ask..

Former CEO of Proteus, Andrew Thompson, suggested that AM failed to take-off because of the way drugs are funded in the US, where the system effectively funds healthcare activity. He claimed that AM did the opposite of that, reducing healthcare costs but also reducing healthcare activity and income for hospitals. (Staines, 2020)

Vasudev Bailey, Ph.D., Partner at Artis Ventures, blamed it more on tech push. He said, "Just because you build something and build it well, it doesn’t mean there is a real need for your product in the healthcare ecosystem or it’s what the end-user wants. Pharma cares about non-compliance, but why should patients care?” (Landi, 2020)

Archimedic's Take

We believe the Proteus flop comes down to healthcare economics. As suggested above, the clinical benefits delivered by Proteus were clear. Reduced hospitalizations and improved medication adherence.

But who's flipping the bill for Ablify Mycite?

It's CMS and private insurance. And what do they care about? Improved healthcare costs, in aggregate. Proteus reduced psychiatric hospitalizations, which is part of the cost equation. But, is that the whole story?

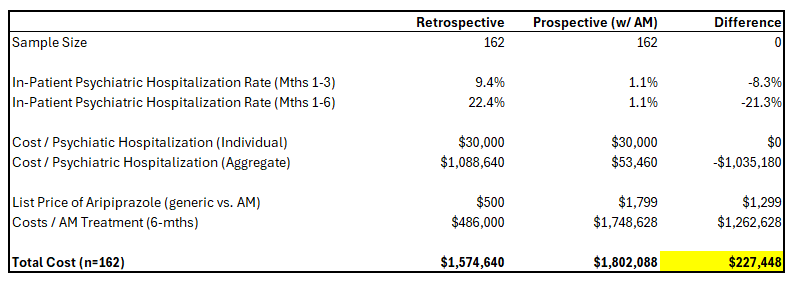

Here's a table to break it down:

Healthcare economic analysis based on psychiatric hospitalization rates from clinical study (Cohen, 2022) and psychiatric hospitalization costs (Haddad, 2012)

Healthcare economic analysis based on psychiatric hospitalization rates from clinical study (Cohen, 2022) and psychiatric hospitalization costs (Haddad, 2012)From the published clinical study (Cohen, 2022), the in-patient psychiatric hospitalization rates dropped by 21.3% when using Ablify Mycite. But, there are a couple of other key data points to consider:

- Costs of psychiatric hospitalization - This ranges from $10k to $50k. An average of $30k is represented in the table above for each incident. (Chen, 2021)

- Costs of aripiprazole - The generic (non-digitized version) has a list price of $500 for a 30-day supply. The AM (digitized version) has a list price of $1799 (drugs.com).

When you multiply psychiatric hospitalizations by the average cost per hospitalization, you land at a savings of approximately $1mm for the AM group. Not bad.

But, let's look at the costs of aripiprazole. Remember, these costs are applied to every single patient, not just the ones that experienced a hospitalization. The smart pills come at a steep premium (approximately 2.6 times the generic). For the clinical study population, the aggregate costs (based on list prices above) are $486k for the generic version and $1.748m for the digital AM version. That's a delta of $1.262M -- a big financial difference for a small sample size.

The healthcare economic argument should be:

$ Robot Pills + $ Reduced Hospitalizations << $ SOC

Well, based on this analysis, the opposite is true.

If you add up the total costs for the Standard of Care (SOC) group, represented by the retrospective study, you'll land at $1.56M. If you add up all the total costs for the AM group, represented by the prospective study, you land at $1.8M.

So, Ablify Mycite (AM) delivers a clinical value prop (reduced hospitalizations) but adds $240k in Total Costs, due to the premium drug pricing. That's a 15% bump over the SOC. Multiply that 15% by the larger patient population, and it amounts to a very big number. Not exactly what CMS and private insurers want to see..

Archimedic’s Analysis: Why Proteus Ultimately Failed

They could have dropped their pricing to deliver a stronger business case to payors. But the price drop would need to be significant. It's not just about hitting breakeven; CMS and private insurers want their share of savings too. There needs to be some incentive on the payor side to justify new coding, coverage, and all the other inefficiencies that come with change.

But, by the time this all happened..

- Proteus was burning $2M per month

- Their product was fundamentally more complex and expensive than generic pills -- hardware (smart patches), software (mobile phone apps, cloud infrastructure), humans monitoring patients -- this all requires resources to build, maintain, and refine

- Otsuka wanted their cut for introducing sensors into their pills

- And Proteus had already burned ~$500M

Changes to the pricing model would've had a cascading effect on the business model, profitability, valuations, and the like.. Investors grew increasingly leery about the viability of the business.

They cut their losses and bailed.

Conclusions

It's important for pharma, medtech, and digital health to drive clinical benefits. That's obvious. But that's not enough. It's equally important to deliver a compelling economic value proposition to the paying customer. That's what I believe the Proteus story tells us.

As developers of new technologies, drugs, and combination products, we are often focused on implementing solutions. Designing, innovating, prototyping, testing, manufacturing, and seeing our ideas come to life. That's the fun part. But, most of the time we should...

Start with a spreadsheet. Lay out the baseline data, the known costs, the expected improvements. Treat the product as a financial model. Ultimately, that's what it is. If you can't get the business case to work in Excel, you're not going to get it to work as a physical device or drug.

Caveats & Credits

There's a lot to unpack with the Proteus story. My cursory review most certainly missed key details, insights, and important perspectives. I welcome those that know about this story to chime in through the comments below. Let loose your questions, comments, and criticisms. If this brief article stimulates some discussion and collective learning, that's a win in my book.

And also, even though Proteus was an epic fail, there's a lot to admire about this product and the team that made it real. They went big and delivered on an amazing vision to fix a huge problem in healthcare. Hindsight is indeed 20-20, and if this was an easy fall to predict in advance, Proteus would not have raised the funds that they did. I don't think this concept is going away, and the Proteus team had an instrumental role in getting it to where it is now. Otsuka has now taken the reins, and I am very curious to see how they get it to the next level.

MedTech companies don't fail because the tech isn't good enough -- it almost always is. Failure comes down to MedTech-Market Fit.

Strong technology and clinical outcomes aren’t enough without a viable economic case. Archimedic helps MedTech and digital health teams evaluate clinical, regulatory, and market fit early. Contact us to discuss your program.

References

To dig in deeper, here are the sources that I used in developing this article:

- Cohen EA, Skubiak T, Hadzi Boskovic D, Norman K, Knights J, Fang H, Coppin-Renz A, Peters-Strickland T, Lindenmayer JP, Reuteman-Fowler JC. Phase 3b Multicenter, Prospective, Open-label Trial to Evaluate the Effects of a Digital Medicine System on Inpatient Psychiatric Hospitalization Rates for Adults With Schizophrenia. J Clin Psychiatry. 2022 Apr 11;83(3):21m14132. doi: 10.4088/JCP.21m14132. PMID: 35421287.

- Chen E, Bazargan-Hejazi S, Ani C, Hindman D, Pan D, Ebrahim G, Shirazi A, Banta JE. Schizophrenia hospitalization in the US 2005-2014: Examination of trends in demographics, length of stay, and cost. Medicine (Baltimore). 2021 Apr 16;100(15):e25206. doi: 10.1097/MD.0000000000025206. PMID: 33847618; PMCID: PMC8052007.

- Haddad PM, Brain C, Scott J. Nonadherence with antipsychotic medication in schizophrenia: challenges and management strategies. Patient Relat Outcome Meas. 2014 Jun 23;5:43-62. doi: 10.2147/PROM.S42735. PMID: 25061342; PMCID: PMC4085309.

- Litvinova O, Klager E, Tzvetkov NT, Kimberger O, Kletecka-Pulker M, Willschke H, Atanasov AG. Digital Pills with Ingestible Sensors: Patent Landscape Analysis. Pharmaceuticals (Basel). 2022 Aug 19;15(8):1025. doi: 10.3390/ph15081025. PMID: 36015173; PMCID: PMC9415622.

- Staines, R. (n.d.). Former CEO of Proteus reflects on the dramatic fall of “digital pill” unicorn. Pharmaphorum. https://pharmaphorum.com/news/former-ceo-of-proteus-reflects-on-the-dramatic-fall-of-digital-pill-unicorn

- From big deals to bankruptcy, a digital health unicorn falls short. Here’s what other startups can learn from Proteus. (2020, September 4). Fierce Healthcare. https://www.fiercehealthcare.com/tech/from-billions-to-bankruptcy-proteus-digital-health-fell-short-its-promise-here-s-what-other

- Proteus raises $17.5M to commercialize its “intelligent medicine.” (2015, December 1). MobiHealthNews. https://www.mobihealthnews.com/17332/proteus-raises-17-5m-to-commercialize-its-intelligent-medicine-platform/

- Perriello, B. (2016, April 18). Proteus Digital Health lands $50m Series H round. MassDevice. https://www.massdevice.com/proteus-digital-health-lands-50m-series-h-round/

- Perriello, B. (2016b, April 18). Proteus Digital Health lands $50m Series H round. MassDevice. https://www.massdevice.com/proteus-digital-health-lands-50m-series-h-round/

- Abilify MyCite Prices, Coupons, Copay & Patient Assistance. (n.d.). Drugs.com. https://www.drugs.com/price-guide/abilify-mycite

- Proteus Digital Health raises another $52 million for sensor-enabled. (2015, December 1). MobiHealthNews. https://www.mobihealthnews.com/35255/proteus-digital-health-raises-another-52-million-for-sensor-enabled-pharmaceuticals/

Support for MedTech at Every Stage

Archimedic partners with medical device teams to solve complex design, development, regulatory, and go-to-market challenges.

Author